Converging pressures from automotive lightweighting and Industry 4.0 adoption are poised to double the global cutting and bending machine market over the next decade, reshaping procurement strategies and supply chain architectures across the metalworking sector. The market is projected to grow from USD 10.2 billion in 2025 to USD 20.3 billion by 2035, at a CAGR of 7.1%, according to Future Market Insights. Automotive OEMs and their Tier 1 and Tier 2 suppliers are the primary demand drivers, as emissions regulations compel a structural shift toward advanced high-strength steels and aluminum-intensive body architectures requiring higher-precision forming and cutting capability.

Background

The acceleration follows years of incremental automation investment, but the pace is now dictated by an EV-driven materials transition. Automotive lightweight materials are projected to grow from USD 88.7 billion in 2025 to USD 147.0 billion by 2030 at a 6.5% CAGR, with metals and alloys holding a 45% segment share, according to DataM Intelligence. The underlying physics are well established: a 10% reduction in vehicle weight yields approximately 6-8% improvement in fuel economy, a figure cited by Market Research Future - and for battery electric vehicles, that same weight saving extends range by a comparable margin. Regulatory context reinforces the investment case. The U.S. Corporate Average Fuel Economy (CAFE) standards and European CO₂ fleet targets have driven OEMs to accelerate multi-material body-in-white designs, integrating advanced high-strength steel, aluminum alloys, and composites into structural components.

Processing these materials at production volumes demands equipment capable of holding tighter dimensional tolerances than conventional mild steel requires. In the automotive sector, lightweighting trends - particularly the use of advanced high-strength steels and aluminum - are driving demand for high-precision laser cutting and press brake systems, according to IndexBox.

Details

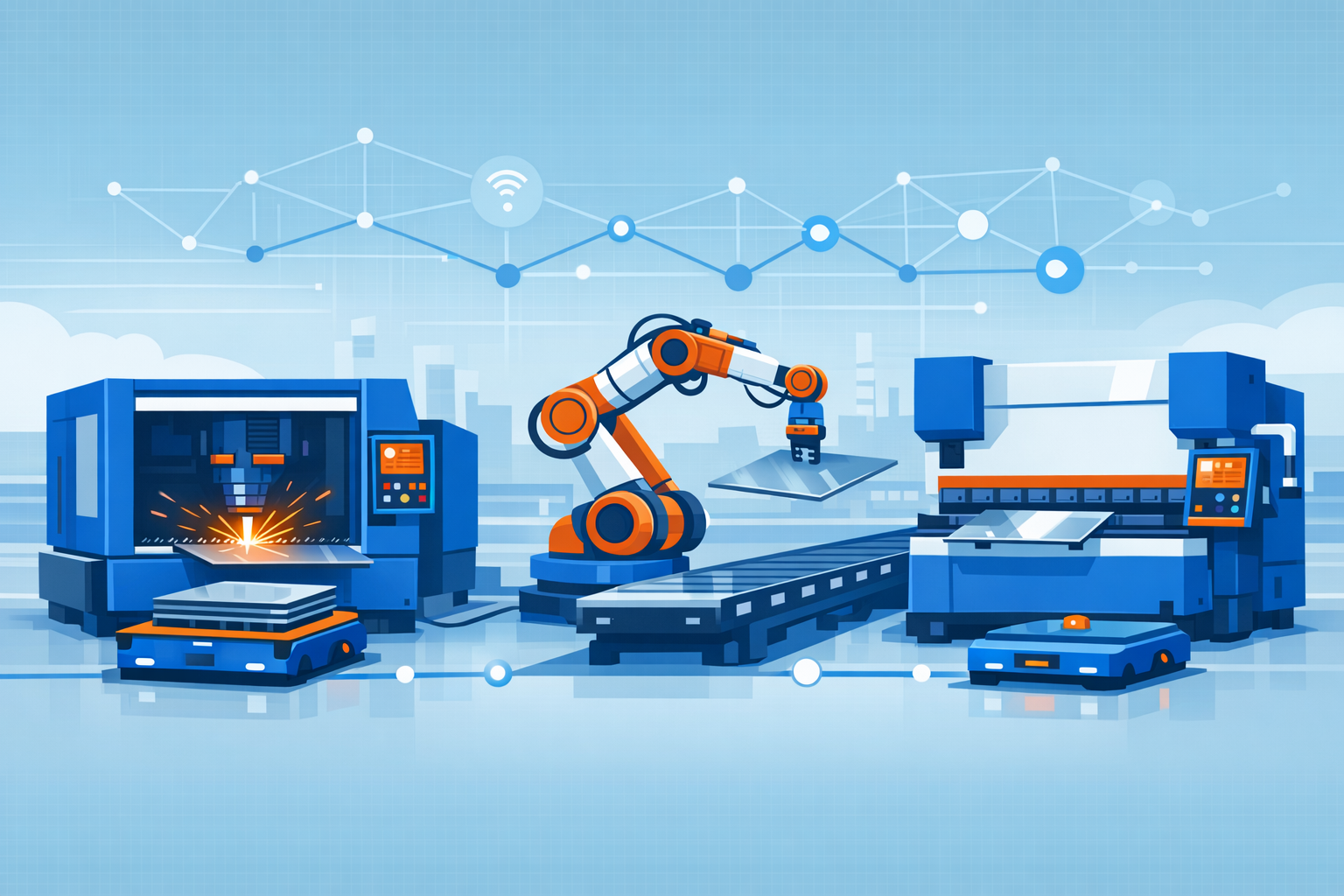

Laser cutting is the most active segment for capital deployment. The global laser cutting machines market is projected to grow from USD 6.9 billion in 2025 to USD 14.3 billion by 2035, registering a CAGR of 7.6%, according to Future Market Insights. AI-assisted programming enables improved accuracy, reduced downtime, and predictive maintenance, making manufacturing processes more efficient and scalable, according to the same analysis. On the press brake side, top-tier flagship models now feature laser angle measurement systems that detect deviations in real time during bending and adjust forming force via AI algorithms, with reported scrap rate reductions of over 80% when working with specialty alloys, according to ADH Machine Tool. Fully electric press brake technology - offering more than 50% energy savings, at least 30% faster operation, and repeat positioning accuracy up to ±0.002 mm compared with traditional hydraulics - has become a baseline expectation among tier-one equipment buyers by 2025.

At the system integration level, automated bending cells demonstrated at FABTECH 2025 featured AGVs transferring blanks directly from laser cutting stations to press brakes, with automatic storage and retrieval systems feeding multiple laser platforms simultaneously, as reported by The Fabricator. Smart sensor packages for real-time performance monitoring, cloud-enabled production data analysis, and predictive maintenance algorithms reducing equipment downtime are now considered standard Industry 4.0 features in new bending equipment.

Geographic demand is bifurcating between replacement and greenfield investment. Germany's cutting and bending machine market is forecast to grow at a CAGR of 6.8%, driven by widespread Industry 4.0 adoption and demand for technologically integrated solutions aligned with stringent manufacturing standards, according to Future Market Insights. The United States accounts for nearly 70% of North America's market share and is projected to grow 1.9 times by 2035, fueled by automotive sector expansion and increasing automation deployment. Asia-Pacific leads on volume, with China projected to record the highest regional growth rate, supported by strong automotive production and increasing investment in intelligent manufacturing technologies.

The divide between large OEM-tier fabricators and small-to-medium enterprises represents a structural tension in the market. Demand is bifurcating between high-volume, low-mix systems for cost-sensitive production and highly flexible, precision machines enabling mass customization and rapid product changeovers, according to IndexBox's automated bending machine forecast. For SMEs, equipment finance structures and leasing models are increasingly central to capital access decisions, as upfront costs for fully connected press brake cells and fiber laser systems with automated material handling remain prohibitive without staged investment pathways.

Outlook

The period between 2030 and 2035 is expected to contribute 56% of decade-long market expansion in double-linkage bending systems, with seamless integration into MES and factory-wide digital ecosystems driving that acceleration, according to Future Market Insights. Interoperability standards for machine data exchange - including OPC-UA and MTConnect protocols - are expected to become procurement requirements at large automotive assembly complexes, raising the compliance bar for mid-tier equipment suppliers. Workforce implications are also emerging: AI-assisted setup reduces reliance on experienced operators for parameter programming while simultaneously increasing demand for personnel capable of maintaining sensor hardware, calibrating vision systems, and interpreting predictive maintenance analytics.